AUDITOR GENERAL'S ANNUAL REPORT

ON THE ACCOUNTS OF SIERRA LEONE 2011

4.3. Some Comments on the Public Accounts

I have issued my Auditor’s Report on the Public Accounts of the Government of Sierra Leone in accordance with Section 119(2) of the Constitution of the Republic of Sierra Leone 1991 and Sections 62 to 66 of the Government Budget and Accountability Act 2005. A copy of my Audit Report precedes the Financial Statements of the Government of Sierra Leone and the Notes thereto which are reproduced in full above.

The financial statements are an expression of the Government’s accountability to Parliament and civil society on how well it has exercised its responsibilities as custodian of the public purse. It is a basic tenet of our system of government that no revenue or expenditure may be collected or spent except as authorised by a parliamentary vote. Therefore the Public Accounts are a report on the extent to which the Government has complied with the intent of Parliament.

The short-form Auditor’s Report – in this instance a disclaimer of opinion - is an expression of professional judgement and its form is dictated by international good practice. I may issue an unqualified, qualified, disclaimer or an adverse opinion. An unqualified opinion arises where the financial statements provide a true and fair view of financial position and performance and a disclaimer arises where the auditor is unable to form an opinion one way or the other. An adverse opinion arises where issues in the financial statements are so pervasive that they do not present a true and fair view. Either a disclaimer or an adverse opinion is a very serious matter.

This year I have expressed a disclaimer of opinion on the Public Accounts. In summary the issues giving rise to the disclaimer are:

Material uncertainty over domestic revenue due to:o significant receipt books not available/accounted for;

o unidentified cash balances held in transit accounts not transferred to the CRF at year end; and

o a significant discrepancy between NRA reported revenue and that disclosed in the Public Accounts.

Material uncertainty over donor revenue as no breakdown was made available for audit.

Material uncertainty over other charges expenditure due to lack of supporting documentation made available.

Material uncertainty on the amount of Project Implementation Units not included in the accounts.

Material uncertainty regarding the disclosure and valuation of miscellaneous debtors and investments.

Material uncertainty regarding the accounting for and consequently the amount of Public Debt.

Material error in non-disclosure of domestic revenue arrears as required by GBAA 2005.All of the matters raised above are developed and commented upon more completely below including my view that Note 2(a) to the Financial Statements, referring to the basis of preparation of the accounts, may well be misleading to readers. This was not mentioned in my disclaimer of opinion but might well have been.

Unfortunately in recent years disclaimers or qualified opinions on the Public Accounts have been the norm in Sierra Leone. Neither the disclaimer nor the matters giving rise to it should be taken lightly and it is unfortunate that despite my concerns expressed in last year’s Annual Report, the matters raised then were largely not acted upon more effectively or completely. While public financial management is improving slowly, I would say too slowly, in matters of internal control around banking and cash management, of both the expenditure and revenue, there remain very serious weaknesses. The accounts are prepared on a cash basis – which I comment upon further below – so it follows that financial reporting is unreliable if controls over banking and cash management are poor. The audit findings are extensive and make poor reading. They are more extensive than in previous years because the audit coverage is greater – it has risen from 63% of expenditure in 2006 to 81% in 2011. In addition, the technical capacity of my auditors has improved and this combined with the increased coverage means there will be more findings, keeping in mind that it appears there is plenty to find.

The following paragraphs set out in greater detail our findings while conducting the audit and the matters giving rise to the disclaimer of opinion.

4.4. Cash and Bank

There has been an improvement in terms of the number of audit confirmations of balances received from commercial banks. Out of a total of Le 63,442 million presented as cash and bank balances with commercial banks for the 2011 Public Accounts approximately Le 32,426 (about 51%) of the total was confirmed directly. This is a marked improvement compared to last year when less than 0.1% of the total was confirmed directly by the banks.

However, we noted discrepancies between the confirmed balances and the disclosures in the Public Accounts. For instance although we received confirmations from Access Bank, Sierra Leone Commercial Bank , Guaranty Trust Bank and Union Trust Bank we noted that the amounts were not those disclosed in the Public Accounts. The total unconfirmed bank balances totalled Le 32,387 million. Conversely, we noted that some bank balances confirmed by the commercial banks were not included in the Public Accounts.

Some of the departmental bank balances listed in the schedules presented for audit purposes were not included in the list of balances disclosed in the Public Accounts, whilst others were included but the amounts differed from those on the list presented by Bank of Sierra Leone. We were unable to obtain an explanation for the non-inclusion and the differences noted.

We noted that opening departmental cash and bank balances were written off as prior year adjustments. The officer in charge of recording these balances explained that this treatment was because of the inconsistencies of Departments in submitting their financial returns to the Accountant General’s Department.

4.5. Government Record Keeping (Other Charges)

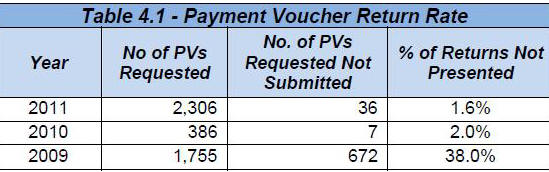

Out of a total of 2,306 payment vouchers for other charges requested 36 were not made available for audit inspection (representing 1.6% of the total PVs requested). This indicates a slight improvement in the percentage returns last year when about 2% of the payment vouchers were not made available for audit inspection. However, in 2009 only 38% was not submitted for audit purpose. This trend is presented in the table below.

We noted that for 108 payment vouchers (PVs) totalling Le 46 billion which were produced for audit inspection that the supporting documentation was insufficient to support the substance of the transaction to which the PVs related. Supporting documents such as invoices delivery notes, certificates of completion or other relevant documents should be reviewed by the Accountant General’s Department prior to payments being made in accordance with section 81(1) of the Financial Management Regulation which states that:

“The Accountant General or authorized officer shall before making any payment against a voucher, check that (a) the voucher is properly supported by the prescribed documents; (b) the documents are attached to the vouchers and are correct and complete in every particular”. The documents should then be filed appropriately to maintain an adequate audit trail. However, during the course of our review of Other Charges, we noted that for payments made by bank transfers, the supporting documents were not attached to the Batch header/payment vouchers.

In addition, we sampled Payment Vouchers for special imprest accounts. Out of these payment vouchers, special imprests amounting to Le 2,211,565,850 were not properly retired by the responsible offices. This represented 67% of the total Payment Vouchers examined.

4.6. Submission of Draft Public Accounts for Audit

I received the draft Public Accounts on the 12th of April, 2012, twelve days past the statutory deadline. Section 57(3) of the Government Budgeting and Accountability Act, 2005 states that:

“The Speaker of Parliament shall, after consultation with the Minister, ensure that the Auditor-General’s copy of the statement of accounts is transmitted to him within the period of three months specified in subsection (1)”.

4.7. Basis of Preparation of the Public Accounts

It is reported in Public Accounts that International Public Sector Accounting Standards (IPSAS) Accrual Standard were used in preparing the Public Accounts with some exceptions. However our audit tests revealed that these standards were not complied with and so the Accountant General agreed that this statement would be changed and it would be reverted to the previous description that the accounts were prepared on a “modified cash basis”. However, even this modified cash basis does not conform to any recognised standard for cash basis reporting such as, for example, International Public Sector Accounting Standard (IPSAS) Financial Reporting Under the Cash Basis of Accounting (Revised 2006).

A basic tenet of all financial reporting, whether in the private or public sectors, is to have a clear view on the boundaries of the accounting entity. That is, to define it clearly. The principle driving public sector accounting is that it should be on a whole of government basis. Defining ‘whole of government’ can be challenging and becomes complex when considering, for example, how to include State-owned enterprises but it is self-evident that all MDAs should be included. When the basis of accounting is on a cash basis it is axiomatic that all bank accounts and other cash balances should be included. Yet for the Public Accounts in Sierra Leone this was not the case.

Note 2(a) to the Public Accounts purports to describe the cash basis on which the accounts of the Government of Sierra Leone are prepared and clearly implies a degree of consistency with the only internationally recognised standard for public sector cash basis reporting, IPSAS Financial Reporting Under the Cash Basis of Accounting. In as much as some bank accounts and balances in transit accounts used by the NRA are not part of the Public Accounts there is a significant deviation from the IPSAS standard and the whole of government principle that renders Note 2(a) untenable. Similarly the reference to IPSAS Accrual Standards – there are over 30 of them – in Note 2(a) is untenable and incorrect. Indeed it is far from clear whether the Accountant General’s Department is fully aware of all bank accounts of the government held in Sierra Leone commercial banks or overseas. My office has not been provided with a comprehensive listing of these bank accounts. Even among those that are known, the balances recorded in the bank statements are not always accurately reflected in the Public Accounts nor, for the most part, is there any reconciliation of the differences. This latter point is raised again below.

We have noted repeatedly throughout this report a failure to observe the most basic control over cash and bank balances, which is that there should be monthly reconciliation of bank statements to accounting records. The implementation of IFMIS, the centralised computer-based accounting system, was a major achievement of public sector reform in Sierra Leone. However, reports emanating from it are only as accurate and reliable as the information contained in its databases. It therefore begs the question if the cash and bank balances are not under control how reliable is financial reporting under any basis let alone a cash basis.

A solid grasp of and a clear definition of the basis of preparation of the Public Accounts sits at the very core of improving the accuracy and completeness of government accounting and financial reporting and needs to be clarified for the Government of Sierra Leone. Without this, capacity building interventions for achieving better financial reporting is destined to fail. We expect to see MoFED and the Accountant General’s Department urgently addressing this matter and it will be an area on which my auditors will focus their attention in the years ahead.

4.8. Project Implementation Units included in the Public Accounts

From our review of the Public Accounts we noted that Project Implementation Units (PIUs) and subvented balances were included in the financial statements, however, from interviews conducted with key personnel in the Accountant General’s Department it was revealed that not all Project Implementation Units(PIU) and subvented agencies balances were included in the financial statements as some did not report to the Accountant General’s Department on a consistent basis.

Project Implementation Units and subvented agencies did not report on a consistent basis thus leading to incomplete figures being presented for consolidation. We were unable to ascertain the accuracy of some of the adjustments made to the accounts in relation to PIUs and subvented agencies.

For example we noted that PIUs and subvented Agencies closing balances for 2010 of Le 206 billion and PIUs and subvented agencies creditors for 2010 of Le 4.7 billion were written off as prior year adjustments in 2011 accounts.

4.9. Miscellaneous Debtors and Investments

A review of the Miscellaneous Debtors and debtors privatisation revealed the following:

The Loan agreement relating to the debt owed by Bumbuna Hydro Electric project for the amount of Le5,213 million was not presented for audit review. The age of this debt and its terms could therefore not be determined. This loan agreement was not provided to us during our previous audits.

A review of the loan agreement relating to SALPOST revealed that interest at a rate of 20% per annum, as stipulated in the agreement, was not computed or recorded in the financial statements.

A review of the debtors schedule, financial statement and loan agreement showed that there were no recoveries made during the year from Bumbuna Hydro Electric Project, SALPOST, Guma Valley Water Company and GAVA Ltd.

A review of the Rokel Commercial Bank Financial Statement revealed that the sum of Le1.3 billion was paid as dividend to minority shareholders. The Government of Sierra Leone share of dividend amounting to Le1.3 billion could not be traced in the Public Accounts and hence not paid to the Government of Sierra Leone.4.10. External Public Debt

External public debts have risen significantly over the years and my auditors carried out extensive work on this area to ascertain that the amounts disclosed are correctly stated.

Audit findings in this area were:

Out of a total of Le2.6 trillion disclosed as disbursed Outstanding Debts in the Public Accounts owed to multilateral and bilateral creditors, only Le767 billion (28%) of this total was confirmed by the external creditors. Although providing external confirmation is not within the direct control of Government, the unavailability of this evidence constituted a significant limitation on the scope of my audit of the Public Accounts. Consequently, I was unable to ascertain whether External Public Debts, disclosed in the 2011 Public Accounts was free from material misstatement.

We carried out alternative procedures to confirm the balances disclosed in the Public Accounts for 9 project (loans), we determined the closing balances and compared those to the balances disclosed in the Public Accounts, we noted a difference of $4,550,249 between the schedules created and the amounts disclosed in the financial statement. This difference represents a net understatement of the balance shown on the financial statements.

The Public Debt Unit did not perform regular reconciliations between the debts in the books of the Government and the amounts shown on the creditors’ statements.

Note 18 (External Public Debts) to the Public Accounts revealed that an exchange loss of Le35 billion was computed by comparing the external public debt schedule submitted by the Bank of Sierra Leone and the schedule prepared by the Accountant General. In my view this is not an appropriate method of determining exchange differences. I was unable to ascertain the correct amount due to insufficient information available during the course of the audit.Prior to the audit of the 2012 Public Accounts, the Accountant General should carry out the following actions:

request all external creditors send in their year-end creditors’ statements; and

ensure that comprehensive reconciliations are performed, comparing and explaining any differences between the debt figures in the Government books and the amounts in the creditors’ statements.4.11. Domestic Supplier Arrears

A review of the Domestic Suppliers Arrears revealed a serious lapse in systems of internal control. There is no control in place to avoid duplicating payments of domestic supplier’s arrears. I observed that obligations relating to Domestic arrears debts amounting to Le406 million, even though settled in 2011 continued to be disclosed in the Public Accounts as outstanding debts.

4.12. Review of the operations and management of the Transit Accounts

The audit procedures to confirm the completeness of revenue collected and banked involved the tracing of receipts issued during the year to the bank statements. My staff was unable to obtain some of the 2011 transit bank statements for all tax streams from the NRA Director of Finance and the relevant Principal Finance Officers especially those related to Customs and Excise department and transit bank accounts denominated in foreign currencies. The Director of Finance indicated that these missing bank statements had not been received from the banks. Consequently, I was unable to obtain sufficient appropriate audit evidence that all revenue received from each tax stream had been banked and transferred to the Consolidated Fund.

Due to the absence of the majority of the transit bank account bank statements, the Principal Finance Officers within the NRA for Customs & Excise, Domestic Taxes, and Non-Tax Revenue departments did not perform a reconciliation of their cash books to the transit bank account statements.

Consequently, due to this failure in a basic internal control procedure I was unable to obtain reasonable assurance that all revenue received had been banked and transferred to the Consolidated Fund.

I confirmed that a year-end reconciliation was performed between the NRA cash book totals for each tax handle (stream) and the Accountant General’s IFMIS system balances (which are based on BSL consolidated fund balances). However, there were differences on the year-end reconciliation which could not be agreed to the transit account bank statement balances at 31st December 2011.

In the case of tax revenue paid in cheques denominated in foreign currencies, such tax receipts may not be shown on the transit bank account statement for up to a month. It could then take up to a further month for such payments to be transferred to the Consolidated Fund.

Furthermore, I attempted to compute the total balances in transit banks not recorded as revenue in the Public Accounts .From the exercise, I ascertained that a total amount of Le 17,167 million was in the Transit Bank statements submitted for audit review at the year end. This amount, i.e. Le 17,167 million is, however, not comprehensive as not all Bank statements were presented for audit inspection, especially bank statements denominated in foreign currencies.

4.13. Review of Revenue Disclosure made in the Public Accounts

The actual revenue balances for a number of tax and non-tax areas contained within Appendix “A” to the Public Accounts were not disclosed in sufficient detail to facilitate comparison with 2011 budgeted line item allocations. For example, there was only one aggregated revenue balance of Le283 billion reported for the whole of Customs & Excise duties. This made it difficult to compare balances both to previous years and to budgeted amounts. Trend analysis cannot easily be done in these circumstances by auditors or anyone else reading the financial statements.

The balances on the transit bank accounts as at 31st of December 2011 should form part of the Public Accounts as stipulated in section 57(5a) of the Government Budgeting and Accountability Act, 2005. Our audit procedure revealed that cash in transit totalling Le5,130 million had not been included in the Public Accounts but is disclosed as a note to the Accounts.